To REBOOT Mercari and its founder Shintaro Yamada, I, Shintaro Tabata, as an individual shareholder with 30,000 shares as of April 24, 2024, propose the following:

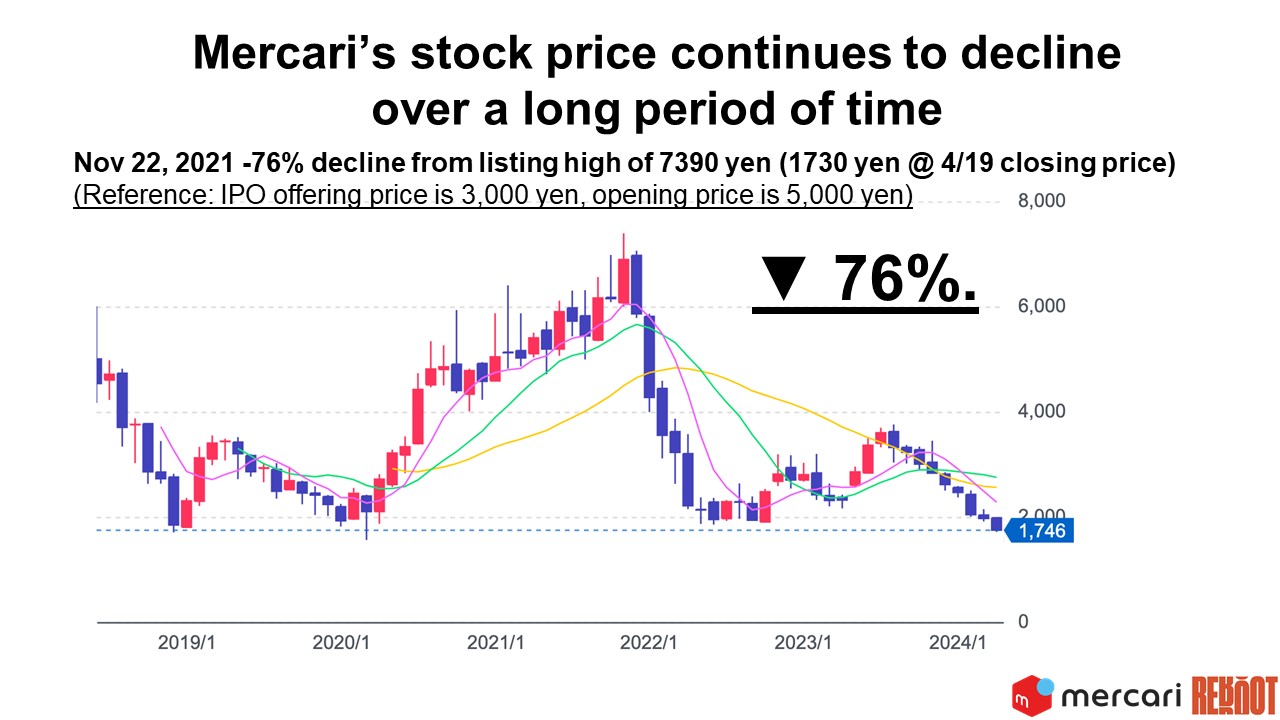

Mercari's stock price has been declining over the long term. As of April 19, 2024, the stock price is 1,730 yen. Compared to the all-time high of 7,390 yen on November 22, 2021, the decline is 76%. It is also below the IPO offer price of 3,000 yen.

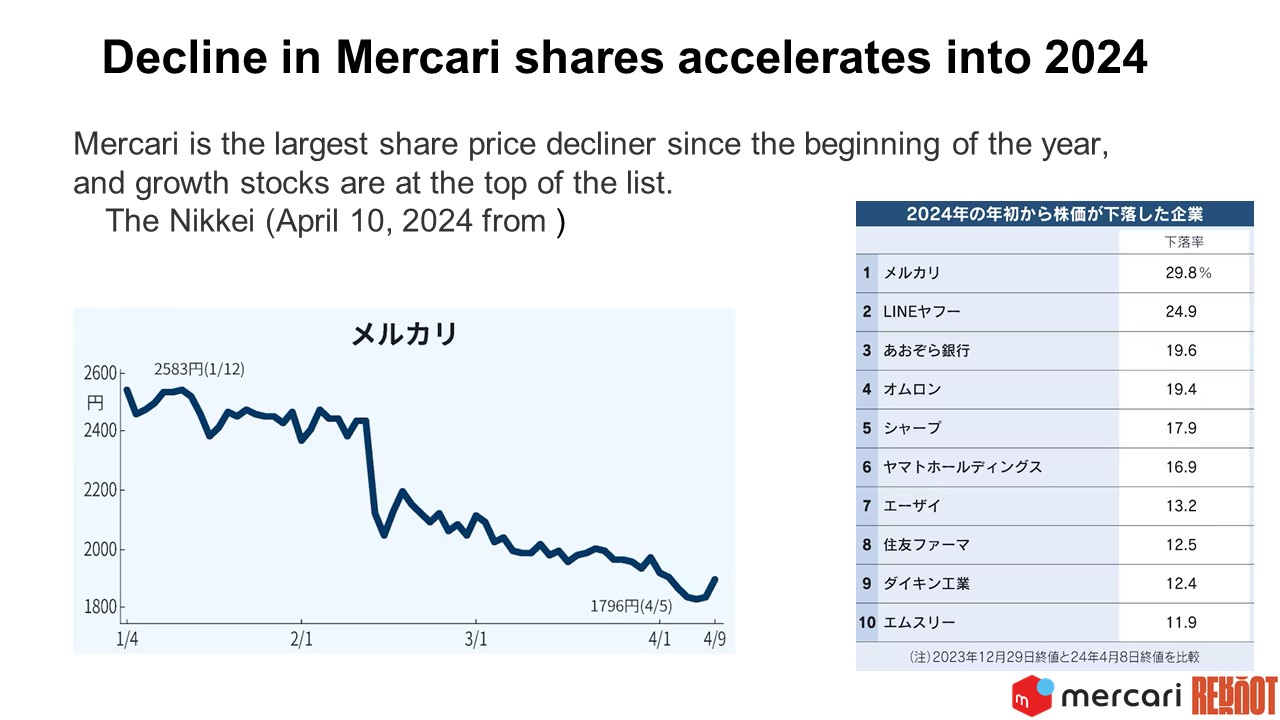

Furthermore, the decline has accelerated in 2024. Despite the historical surge in the Nikkei Stock Average, Mercari's stock continues to fall. Comparing the closing prices of December 29, 2023, and April 8, 2024, the decline rate is 29.8%. The drop in the stock price since the beginning of the year is noted to be the largest for Mercari, as highlighted by the Nikkei Shimbun on April 10, 2024.

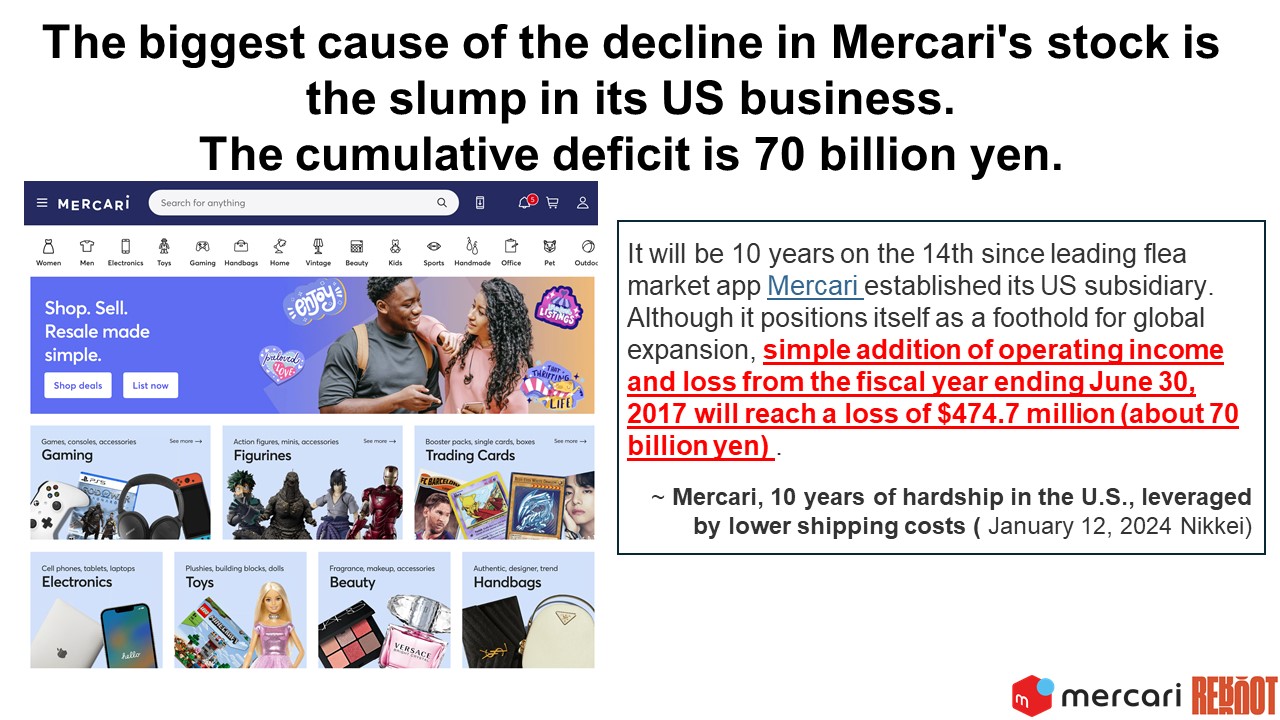

Mercari, the flea market app that boasts an overwhelming 70% market share in Japan, is a household name with its immense popularity domestically. However, there's a factor hindering the smooth growth of its domestic business - its US business. Mercari was founded in 2013, and its US subsidiary was established the following year in 2014.

While it was positioned as a foothold for global expansion, its performance has not been impressive. Ten years have passed since the establishment of the US subsidiary, and the cumulative losses have reached 70 billion yen (simple sum of operating losses from the fiscal year ending June 2017)."

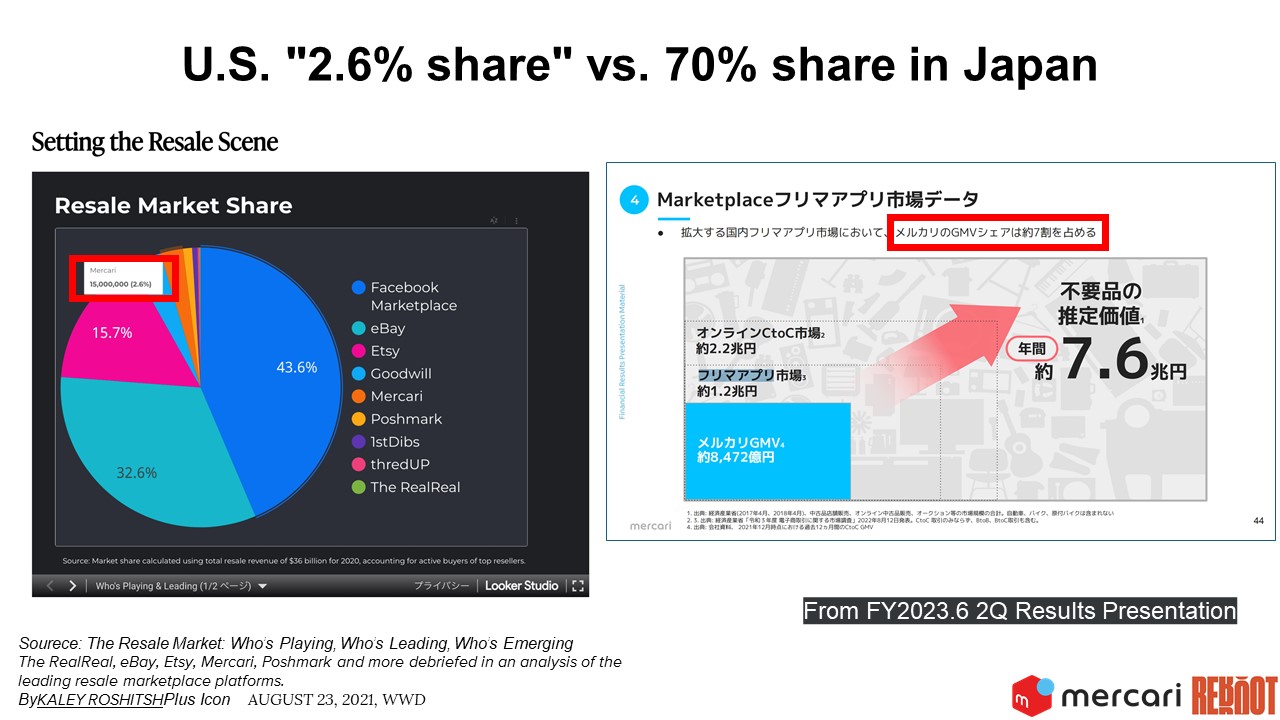

Furthermore, according to a survey by WWD, Mercari holds a mere 2.6% market share in the United States. It significantly lags behind competitors like Facebook Marketplace and eBay.

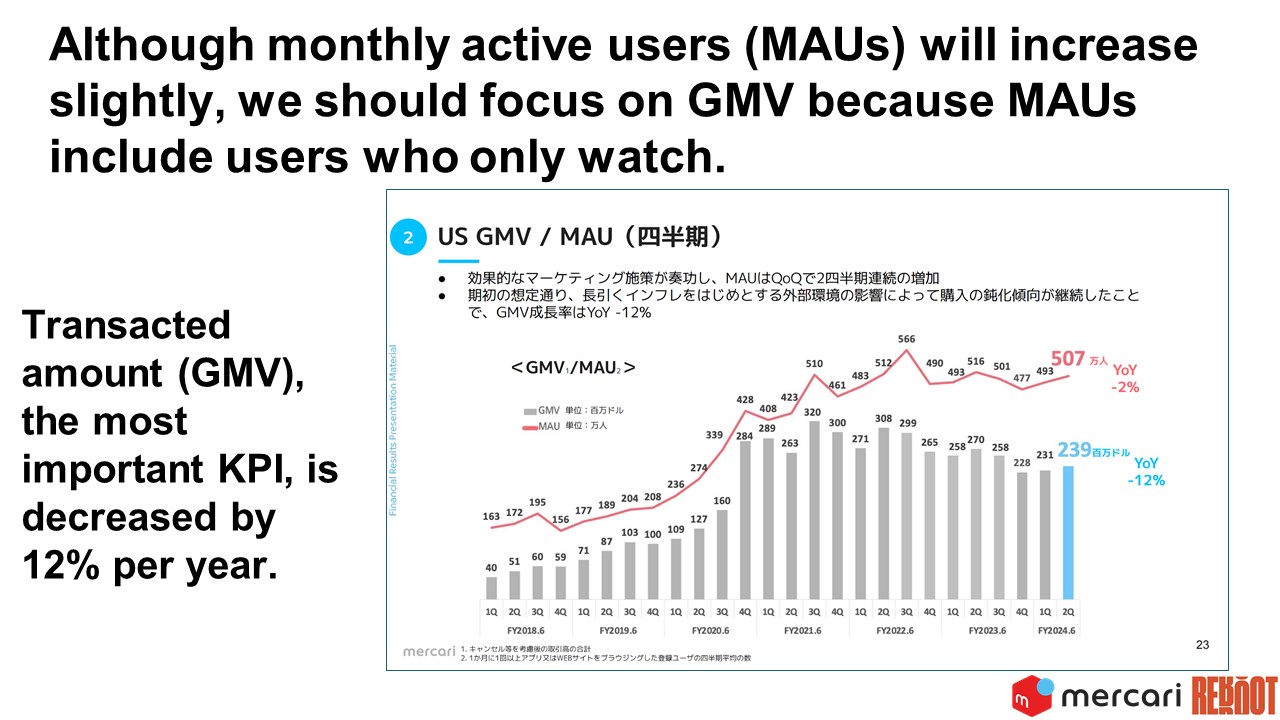

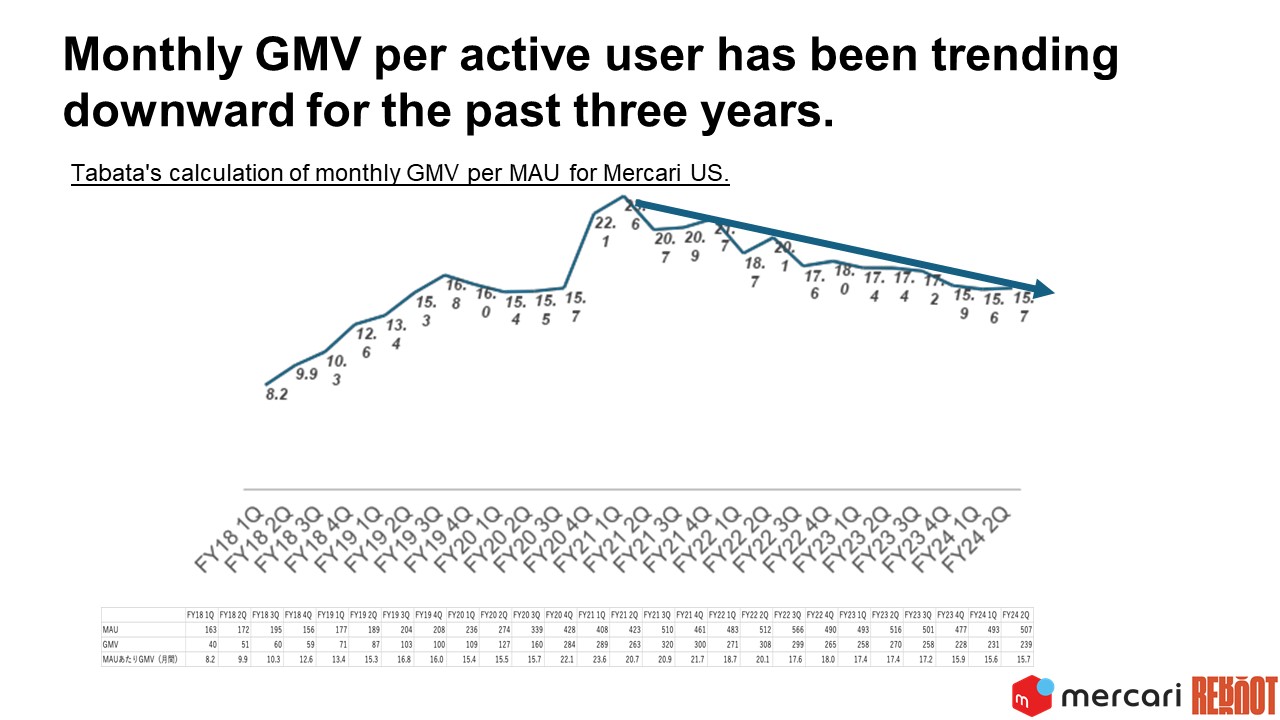

According to Mercari's financial presentation materials, the Monthly Active Users (MAU) for the US operations have been increasing for four consecutive quarters. However, merely increasing the number of 'view-only' users is not meaningful. Therefore, I have been closely monitoring the most important Key Performance Indicator (KPI), Gross Merchandise Volume (GMV). From the MAU and GMV data, I calculated the transaction amount per user. While there was a temporary increase during the COVID-19 pandemic, the downward trend has persisted for three years since reaching its peak.

Mercari continues its US operations, despite the mounting losses and no signs of increased trading activity or expanding market share, because it is a "heart and soul" project of CEO Shintaro Yamada. Since the early days, Yamada has been vocal about creating a "Mercari for the US" and has remained committed to the American market. His vision is to create a service used worldwide, and he believes that if Mercari can succeed in the US, it can succeed globally. It is a business fueled by such dreams and passion.

I think those aspirations are admirable as well. However, what are the results?

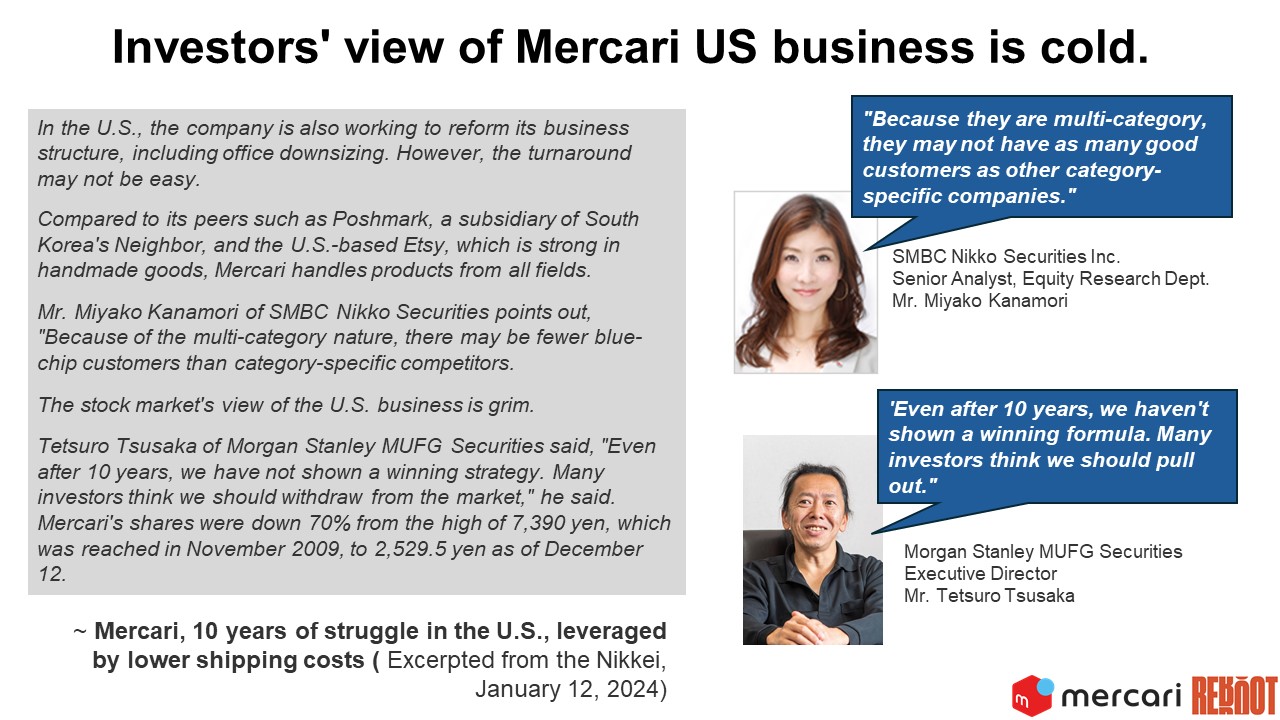

Investors' perception of Mercari is indeed quite harsh. Tetsuro Tsuzaka, Executive Director at Morgan Stanley MUFG Securities, has stated, "Even after 10 years, Mercari hasn't shown a winning streak. Many investors believe it should withdraw."

Tsuzaka had set Mercari's target stock price at 8,000 yen back in January 2022 when Mercari's stock price was at its all-time high. He pointed out that "the growth rate of the US business will determine the future fluctuations in the stock price." The current decline in Mercari's stock price could be seen as a disappointment for investors who had faith in its growth in the US.

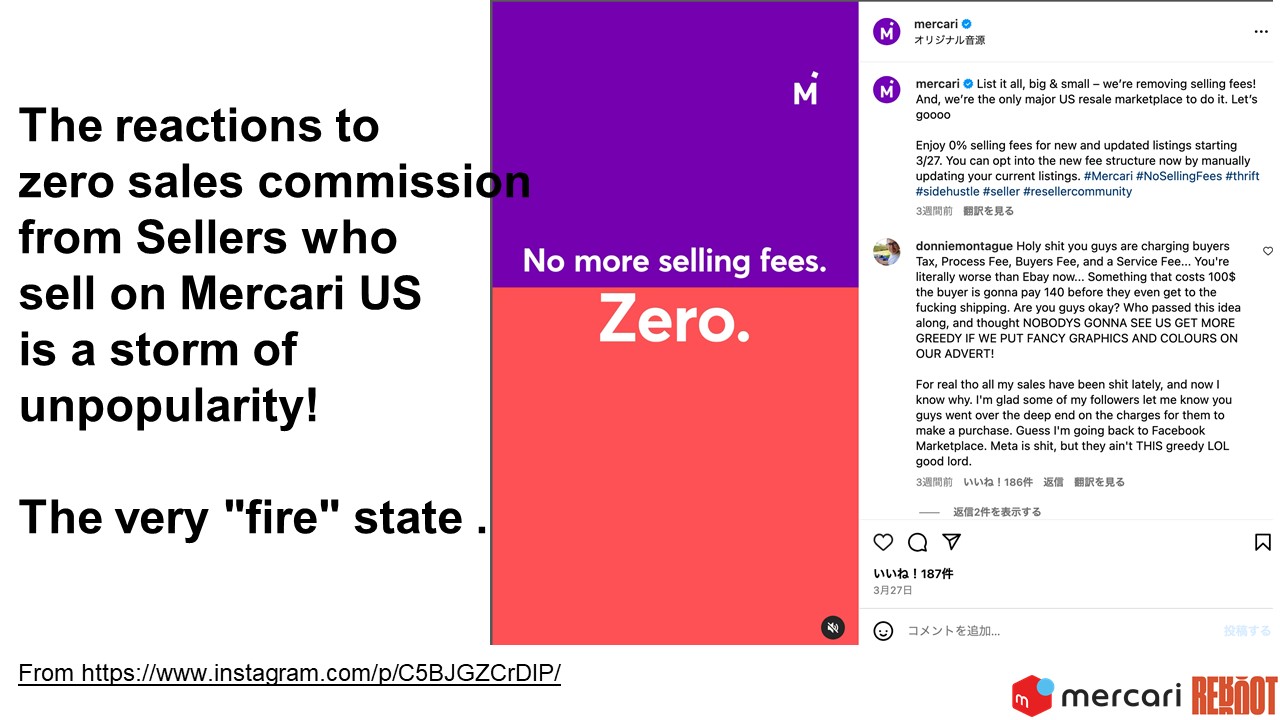

Of course, Mercari is not just leaving its US business untouched. In an attempt to revive the business, they have implemented a "zero sales commission" campaign starting from April, aiming to stimulate transactions. The results of this campaign will be announced in the next earnings report, so it is still unclear at this point. Based on publicly available information, it can be reasonably inferred that the situation is not going smoothly.

Regarding the US business, it seems that Mercari's current strategy is to withstand the situation without making unnecessary investments and to cut costs. It's like being stuck between a rock and a hard place. Unable to reach the summit or retreat to the base, Mercari finds itself enduring a blizzard on the mountainside while trying to conserve resources. However, being a deficit flea market app, simply standing still won't expand its market share. It's evident that continuing to operate at a loss and remaining stagnant will lead to a slow decline.

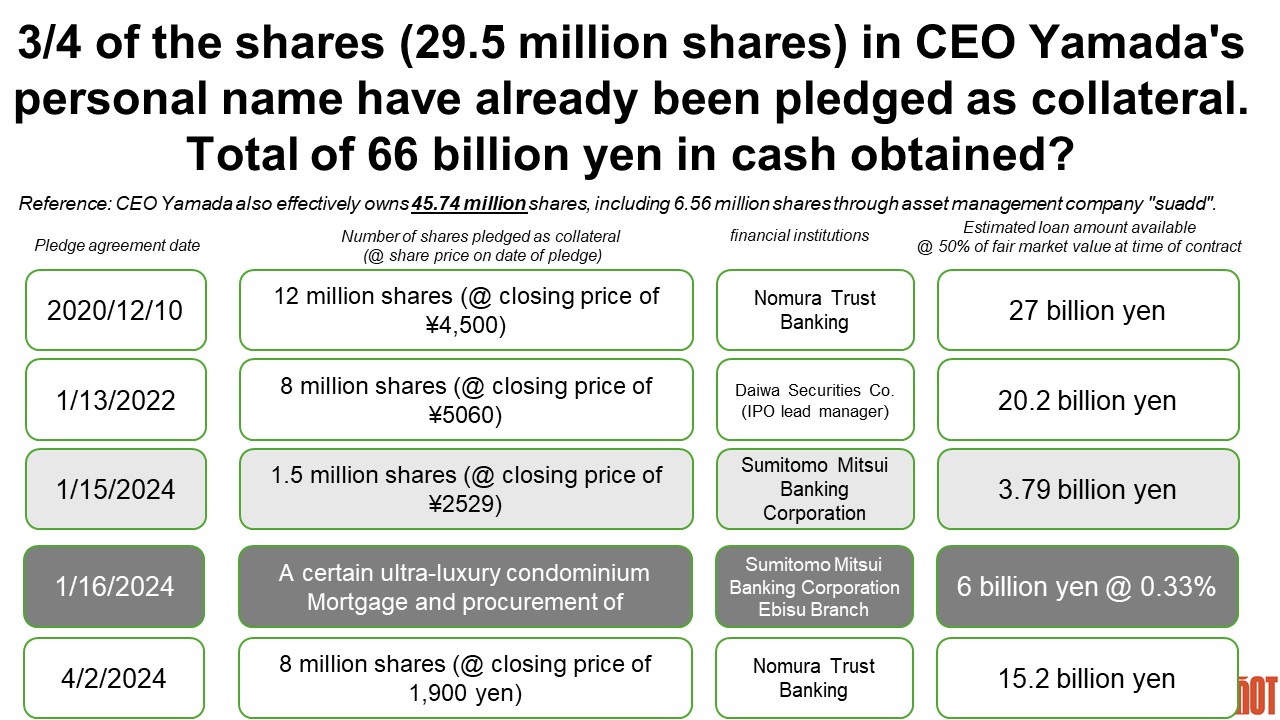

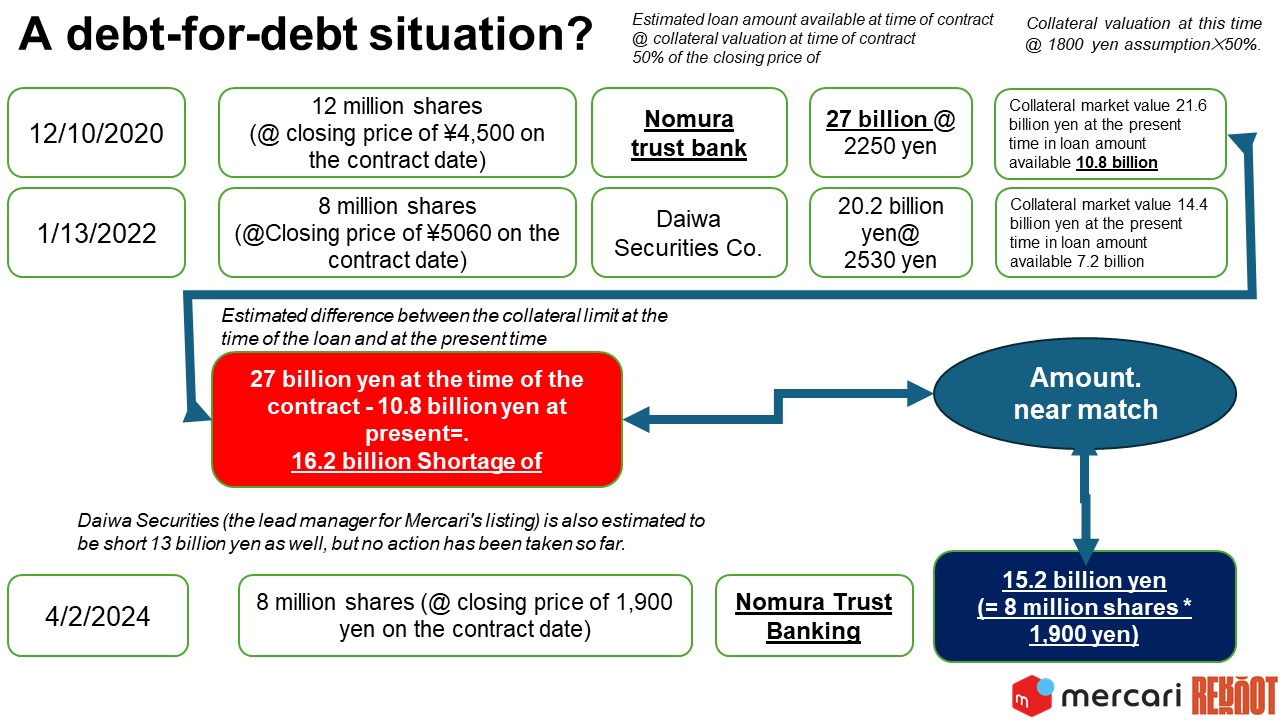

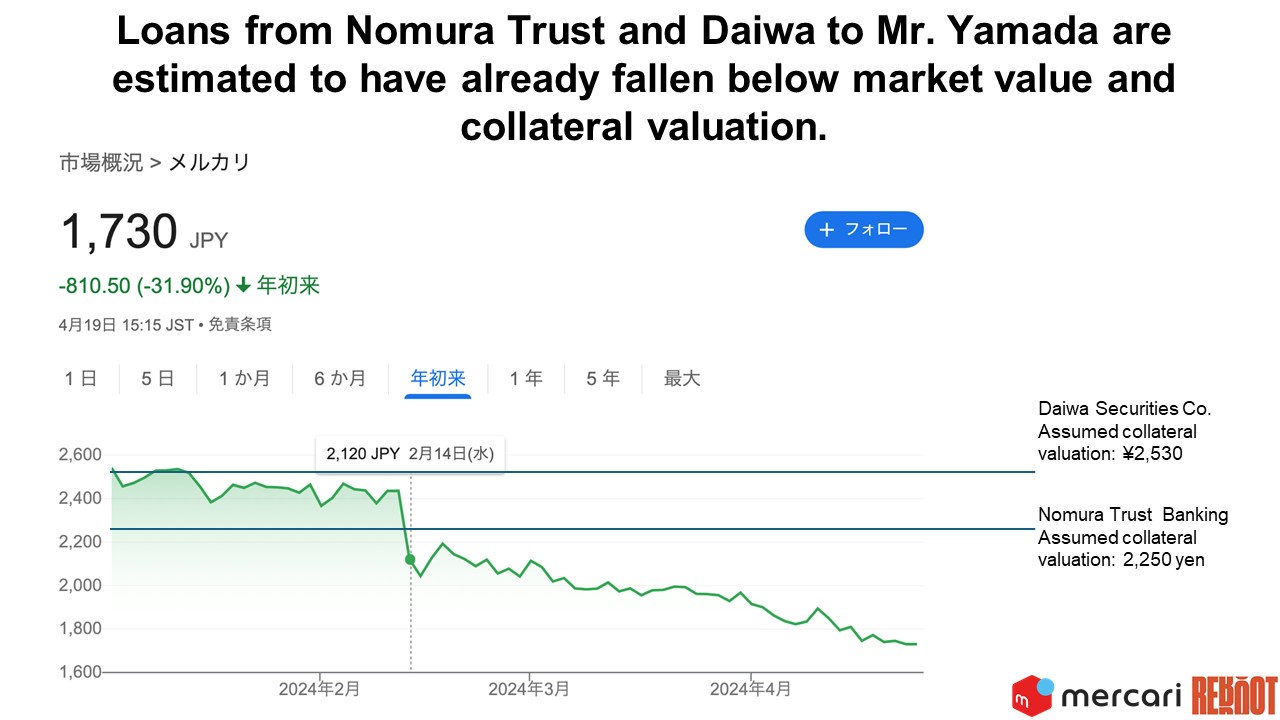

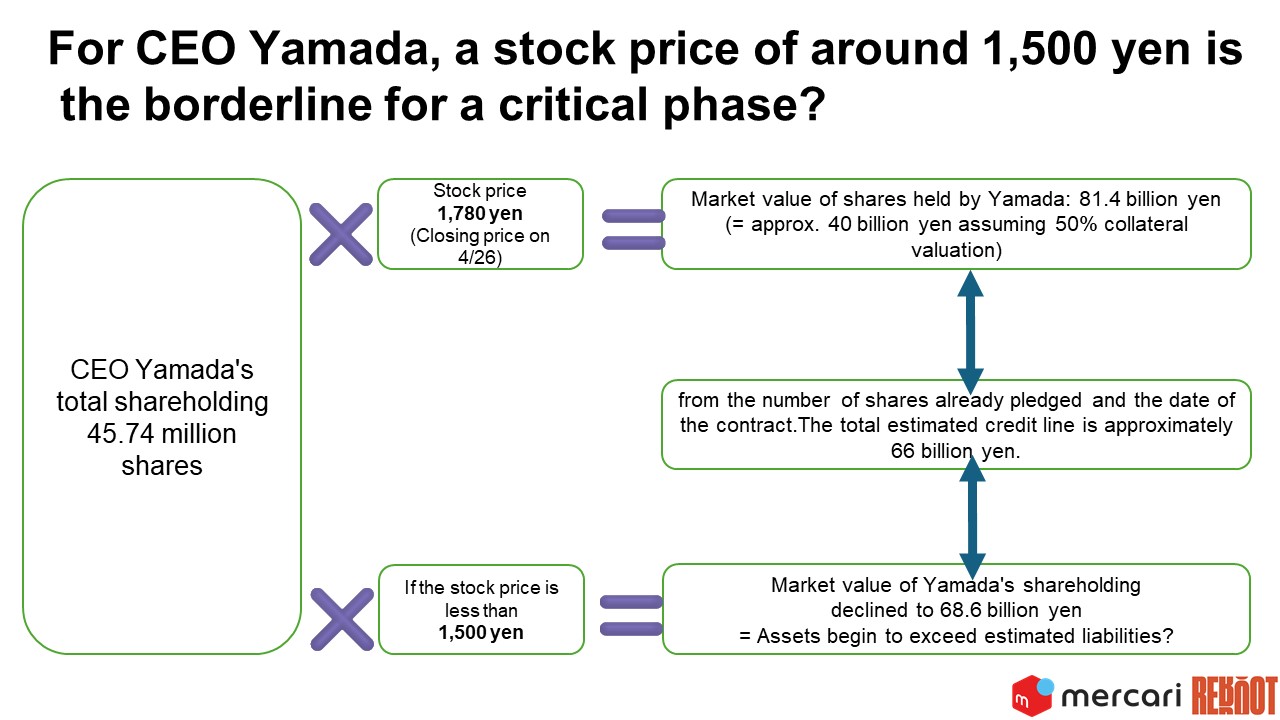

According to the large shareholding report, CEO Yamada has entered into collateral agreements with multiple financial institutions, pledging a total of 29.5 million shares of Mercari stock. While the report only indicates the fact that such a number of Mercari shares have been pledged, it can be inferred from the movement of stock prices and the dates of the collateral agreements that there is a possibility of Yamada being in a situation akin to borrowing to pay off debt.

What I am pointing out to Mercari in this instance is entirely feasible with disclosed information and reasonable inference.However, observing the current situation at Mercari, it seems that the outside directors, who are supposed to represent the interests of external shareholders, are unable to make such observations. As a result, I can't help but wonder if they are fulfilling their roles as directors properly.

Mercari has 10 directors, out of which 6 are independent outside directors. Among these 6, 5 do not hold any shares of Mercari. Without any shares, these outside directors may lack the incentive to advocate for shareholder interests or feel the pain of a decrease in stock price.

Since the establishment of the US subsidiary 10 years ago, we have already incurred cumulative losses of 70 billion yen, with no clear prospects for a turnaround in sight. I urge you to face this reality and make the courageous decision to withdraw from the US business, setting aside the attachment to your persistence since going public.

Furthermore, I request that we concentrate our management resources on the nationwide launch of "Mercari Hallo," which began on April 16th, and devote our full efforts to surpassing our competitor, Timee Inc.

If the US business is to continued, I believe it's necessary to remove John Lagerling, the Executive Vice President in charge of the US business, and have CEO Yamada take direct responsibility for the US business. It's evident that Yamada bears significant responsibility for appointing and supervising an executive who has shown no results for six years.

We request a shareholder return by initiating dividends at around 30% of earnings per share, departing from the no-dividend policy maintained since the IPO. Due to the long-term decline in stock price, it is inferred that CEO Yamada's share-backed loans have already encountered a situation where the market value of the shares falls below the collateral valuation for the first two loans (from Nomura Trust Bank and Daiwa Securities), resulting in collateral deficiency requiring additional collateral injection to rectify.

In addition to the underperformance, there is also the possibility of a financial shock. To prevent further decline in stock price, I request the initiation of dividends as a signaling towards stock price recovery.

Currently, Mercari holds its shareholders' general meeting entirely online. However, ISS has stated that virtual-only general meetings are considered shareholder-unfriendly. Therefore, I request a change to a hybrid format, incorporating both in-person and online elements, for the shareholders' general meeting.

I, Tabata, purchased 30,000 shares in mid-April. Therefore, at the shareholders' general meeting scheduled for September 28, 2024, I will not meet the requirement of holding the shares continuously for 6 months, and thus, I will not be able to make shareholder proposals. If this proposal and the stock price recovery do not materialize, I will continue to monitor the situation with the possibility of making shareholder proposals at the general meeting in September 2025.

Born in Ishikawa Prefecture in 1975. Graduated from Keio University, Faculty of Economics.

In 1999, I joined NTT Data Corporation. Then, i moved to Recruit where I launched the free magazine "R25"; moved to Livedoor in 2005 and subsequently led the management turnaround as Executive Officer and General Manager of the Media Division; managed digital businesses such as VOGUE/GQ at Condé Nast as Country Manager; and in 2012, joined NHN japan; later, served as Senior Executive Officer of LINE, overseeing corporate business before and after the company went public.

Since 2018, I had been working at Start Today (now ZOZO) as an executive officer and head of the Communication Design Office at the invitation of Mr. Maezawa, where I was responsible for public relations and branding.I retired from ZOZO at the end of 2019. Currently, I am a marketing and PR advisor for several different venture companies and have been a private investor for 20 years.

Twitter(X) 350,000 followers

YouTube :160,000 subscribers